Real estate is commonly known as the oldest asset class for good reason. 68% of the world’s wealth exists in real estate, locked up in homes – a basic necessity for life. Homes are also the biggest quantum purchase that one may make in their entire life, and such need to be carefully considered before purchase. As a physical property, real estate also offers unique advantages over other classes of assets such as stocks, bonds, and physical luxury goods. In this article, we cover 7 Unique Traits of Real Estate as an Investment, and help you understand this asset class better. If you are interested in investing in real estate, or are deciding between different investment vehicles, this article might help.

#1 High leverage

Real estate is one of the only asset classes where buyers are expected to use leverage on purchase. Leverage by definition is the use of debt (borrowed funds) to amplify returns. It is akin to borrowing money from your friend at the blackjack table because you feel lucky on the round.

In most other markets, leverage is regarded as highly risky and only offered to privileged individuals. Not only are potential gains multiplied, potential losses are also multiplied by the same factor. In the stock market for example, a broker would not typically allow investors to purchase $10,000 worth of stocks using only $2,500 of cash, and promise to repay the remaining $7,500 at a later date.

However, leverage in real estate is slightly different. Because real estate purchases have huge price quantum, buyers are not expected to pay the full value of the purchase in cash, but instead take out a loan to finance the purchase. For Singapore, the amount able to be leveraged varies by situation and buyer profile, but most first-time home buyers can borrow up to 75% of the total value of the home purchase (in the instance of a bank loan) while putting down 25% in down payment of cash or CPF.

The only restriction on using leverage is that the buyer has to show proof that they are able to repay the monthly installments of the loan. Typically, this is done through showing proof of income and considering all other debts that the buyer may have.

Leverage in real estate is not only generally safe – buyers will only have to take care of the monthly mortgage payments and the interest charged by the bank, but can leverage on the bank’s money to be a part of a debt that can be slowly eroded through inflation. As the value of the dollar gets smaller over the years, the absolute sum paid to the bank remains the same. For example, a monthly mortgage for a HDB flat purchased 30 years ago could stand at a couple hundred dollars per month. Though this was a big sum of money in the past, inflation, which has reduced the value of the dollar, has made this a small amount today. In other words, by leveraging on the bank, inflation can help to erode your debt.

#2 Capital appreciation

Like most other assets that are traded on the market, real estate prices can increase, leading to higher valuations for the property that you own which you can then sell to others for a profit. In land scarce Singapore where homes are always in demand, we can expect capital appreciation for home to generally hold true.

Demand and supply often push the prices of homes up, and an increase in demand for real estate coupled with our dwindling supply have been pushing the prices in the housing market up. This is evident from the sharp increase in price per square foot of new launches today, where we are witnessing increasingly smaller sizes and higher prices, revealing the ever increasing price of land on the side of the developer, reflected onto the consumers. Moreover, increase in construction costs have also pushed property prices upwards, leading to a general capital appreciation in real estate. Scarcity of not only construction materials, but labour, have added to this price tag. For example, in 2021 alone, the pandemic spurred home prices to skyrocket, and the condo resale market saw strong growth across all districts in Singapore.

This, combined with leverage, means that a buyer can put down $250,000 down payment on a $1,000,000 home and if the price appreciates by even 5% ($50,000) over the same year, they would have used the $250,000 downpayment to make $50,000, a 20% return on paper. Of course, this is not accounting for other costs that the buyer will have to bear, such as the interest, as well as stamp duty or legal fees.

#3 Income generation

However, unlike most common assets, real estate is also unique in that it can generate relatively steady and frequent income through rental payments. Buyers have the option of renting out the property, or part of the property (co-living) for a boost to their monthly cash flow. Having extra cash every month allows homeowners to be more flexible in their spending. For example, rental income can be used to repay the mortgage for the same property, to finance another property, or for other spending.

#4 Useable

As an alternative to renting, real estate can also be used for its original function – living in. Like a luxury handbag, watch, or car, a house can be used. In this case, a house can be lived in and is where the majority of one’s time is spent. Here, the property is usable, and provides value to the owner. This use of a property is also flexible, since one can choose to rent it out, or allow other family members to stay in.

#5 Flexible repayment options: Equity Cash Out / Term Loan

Due to the long-term nature of mortgage repayments, there are many options available to homeowners should the value of their property appreciate. Homeowners can choose to do an Equity Cash Out from their current property which provides them with more liquidity on hand. This liquidity then translates to flexibility in terms of long term planning, allowing homeowners to explore other investment options or even getting a second home. Doing so would cause mortgage repayments to extend over a longer period, but can be attractive if the property is continuously increasing in price and buyers want to cash out from their property without having to sell it.

However, there are some restrictions on equity term loans in Singapore. Equity term loans can only be taken out by owners of private properties, and the maximum loan amount is 80% of the property value. More importantly, the amount of CPF used for this property purchase and any outstanding debt is subtracted from the loan amount. The TDSR of 60% also applies unless the total outstanding loan plus new loan amount is less than 50% of the property value.

While these loans may look attractive, they are also highly situational. Equity home loans cannot be paid using CPF unlike other home loans and there are added legal and administrative costs needed to secure the loan.

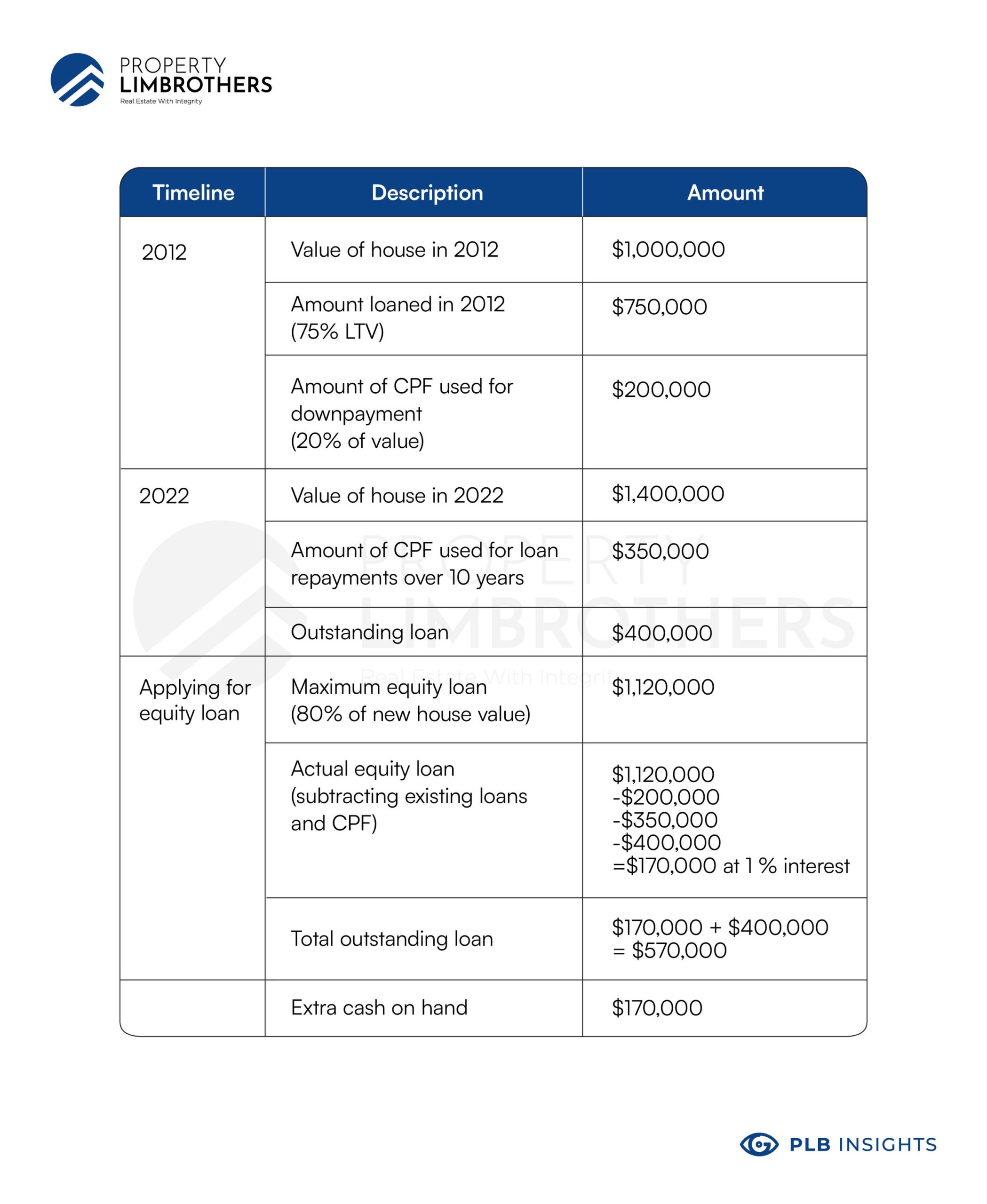

Nevertheless, let us take a look at how an equity term loan is structured:

In 2012 Mr. A buys a house for $1,000,000. 10 years later, the house is now worth $1,400,000 due to price appreciation.

Mr. A has paid off part of the loan and still owes $400,000 of principal.

Mr. A speaks to the bank who are willing to write him an equity term loan of $170,000 based on the following calculations.

The final amount loaned is $170,000 in cash at a very low interest rate. If interest rates were lower when Mr. A refinanced the loan compared to the original loan, it is possible that he ends up paying even less interest overall with the new loan compared to the old one.

Despite the heavy restrictions and extra effort it takes to secure an equity term loan, they can be useful for extracting cash from well-performing properties without necessarily having to sell the entire property.

#6 Debt financing instead of equity financing

The reason all of the previous financing options are available is because real estate is financed with debt and not equity. This means that all profits that are made from price appreciation of the property are kept by the homeowner. The bank is generally disinterested in the profits, and does not share in your profit when your house appreciates in the future.

Here, banks are only interested in making money through stable and predictable repayments. They do this by collecting interest in addition to the principal they lend out. However, should you be unable to pay the loan, the bank is legally allowed to collect the property back as collateral.

This is unlike other equity financing where an investor contributes 25% of the principal and expects to ‘own’ 25% of the asset. Because they own part of the asset, they can then claim 25% of the profits when the asset is sold off, and share in any of your profits. This is more common in businesses than real estate properties.

#7 Illiquid in Nature – Low-Volatility/ Safe Haven

Liquidity is a measure of how fast one can enter and exit the market. Real estate is typically less liquid than other asset classes such as stocks because it is a physical asset (and a large one too!). A property transaction takes anywhere from 3-6 months from start to end. The first 3 months are for marketing, and finding a buyer. The next 3 months are for negotiations and completion of fund transfers and legal contracts.

In addition, there are also many legal clauses bound to a property which complicates the transaction between parties. The liquidity of real estate varies around the world depending on the laws governing the sale and purchase of real estate property. However, Singapore tends to have a less liquid market than most other countries because of our various cooling measures. For example, our residential properties have an illiquidity period of a minimum of 3 years because owners generally would not want to pay Seller’s Stamp Duty which applies for the first 3 years of ownership.

Commercial properties are more liquid because they are not bound by the same measures as residential properties. Nevertheless, the physical nature of real estate combined with the massive price tags associated with each transaction means that transactions are infrequent relative to other assets.

However, illiquidity is not inherently bad as it stabilises the market to provide less price volatility. With lower volatility comes lower price appreciation, but also lowers the risks of a property suddenly losing its value.

This is especially true in Singapore, where the real estate market is regulated by the Singapore government. Here, the many rounds of cooling measures serve to protect the market and prevent a bubble where investors buy beyond their means. Because of this, the market over the years has demonstrated very healthy buying and selling patterns that allow the investors to continue pumping their money in.

This phenomenon of real estate as a safe haven for a store of value, was evident during the pandemic, where foreign investors continued to find ways to buy Singaporean properties despite our high Additional Buyers’ Stamp Duty (ABSD) rates. Holding a general reputation for being highly effective with low corruption, Singapore has made itself a investors’ haven to fund their assets, encouraging foreign clients to purchase local properties as an asset.

Good Debt Vs. Bad Debt

One of the most important concepts we then have to understand about real estate is distinguishing between good and bad debt. While the large investment may seem like a liability, the money pumped into real estate actually acts as a hedge against inflation. When an investor chooses to place his money into real estate, this is an asset class that generally will appreciate and provide returns should he decide to sell it. Understanding the power to leverage, we see how inflation can actually work in our favour, to help us pay off the debt in the long term. This is in contrast to purchasing a property that is guaranteed to depreciate, such as a car, where the money invested will not return to us at the end of the day. But more on real estate as an inflationary asset in Part 2 of this article, Real estate: A unique hedge against inflation!

Conclusion

In conclusion, real estate as an asset has many unique characteristics that make it an excellent store of value. Apart from its usability and illiquidity, properties allow us to leverage on other people’s money to grow our investment. If you are still curious about this phenomenon on asset inflation, be sure to stay tuned to our upcoming article! Till then, we are always open to any questions, or just a quick chat!