Many Singapore property investors assume: “My rental yield is 4%, my loan rate is 3.5%… confirm profitable!”

This is a common misunderstanding.

Gross rental yield may look attractive on paper, but it often masks the true cashflow reality — especially in today’s high interest rate environment.

Let’s break down why.

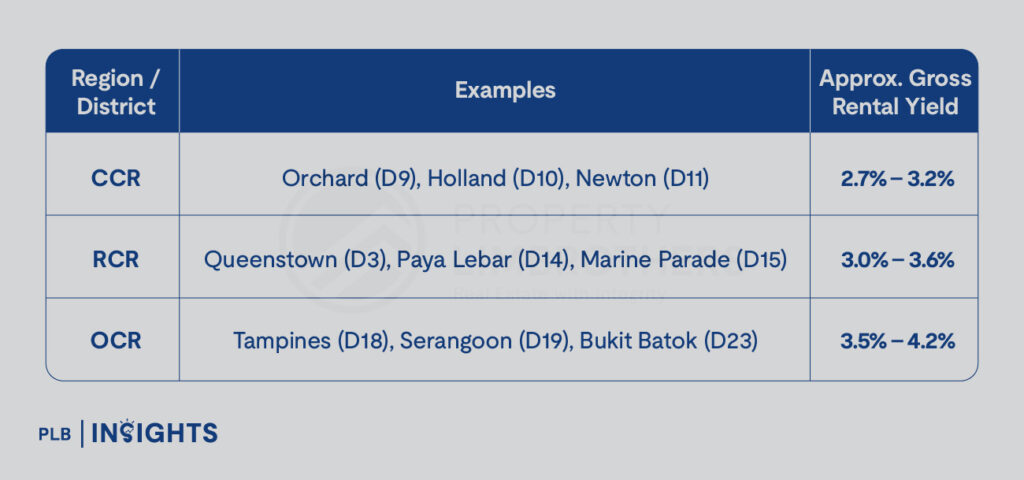

Singapore’s Gross Rental Yields by District

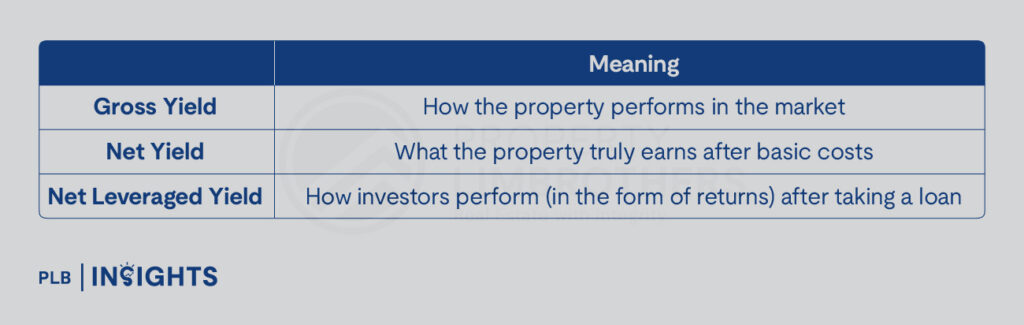

Gross rental yield indicates how the property performs in the rental market, not how much profit you pocket.

Even with a 4% gross yield, you may still see negative cashflow after financing costs.

A Realistic Singapore Example: District 19 (Serangoon / Hougang)

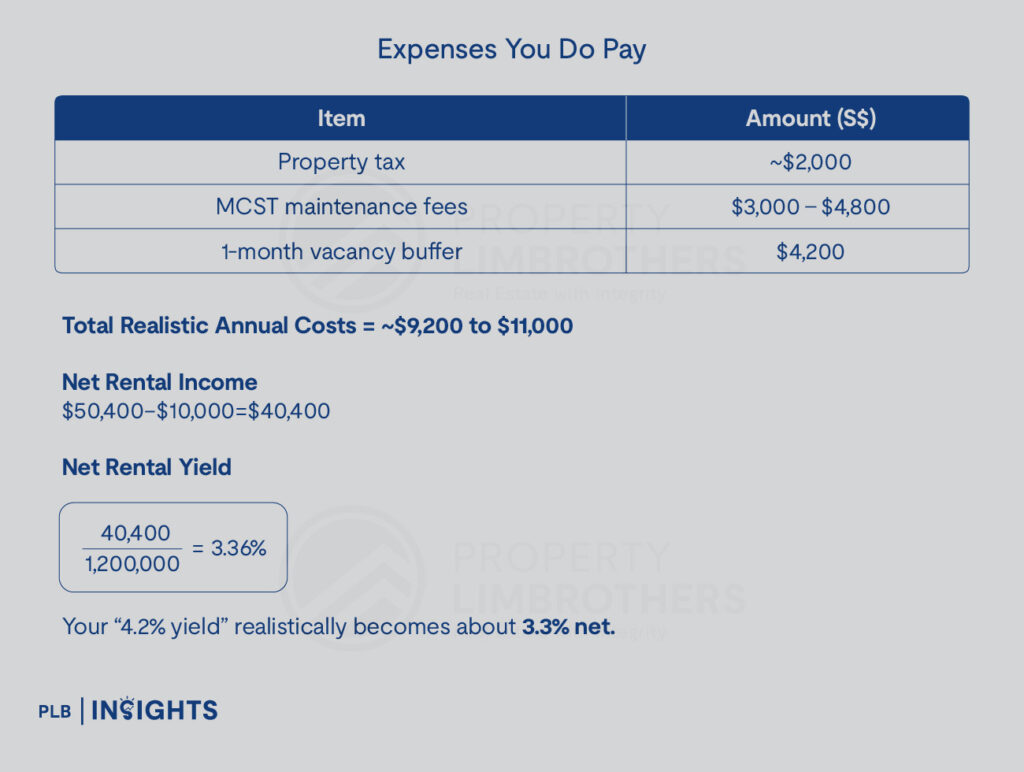

Now let’s remove unnecessary costs and focus on what Singapore landlords almost definitely pay.

Realistic Annual Expenses

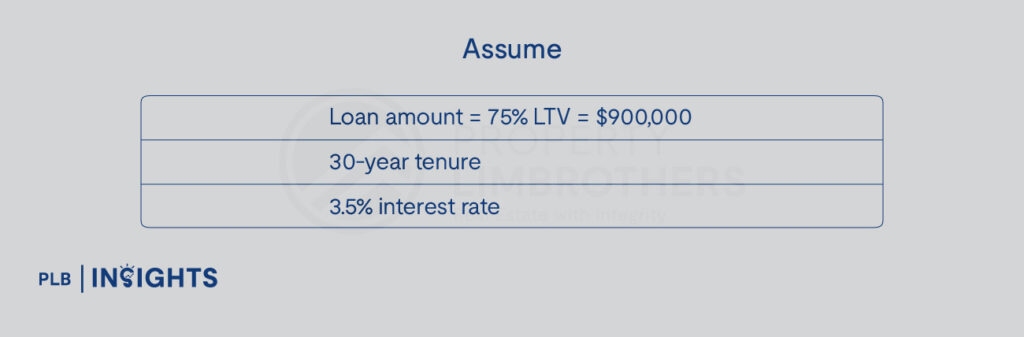

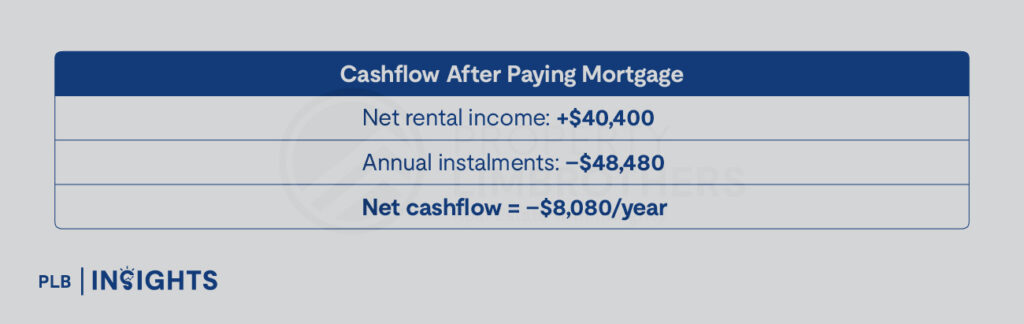

The True Cost: Mortgage Instalments

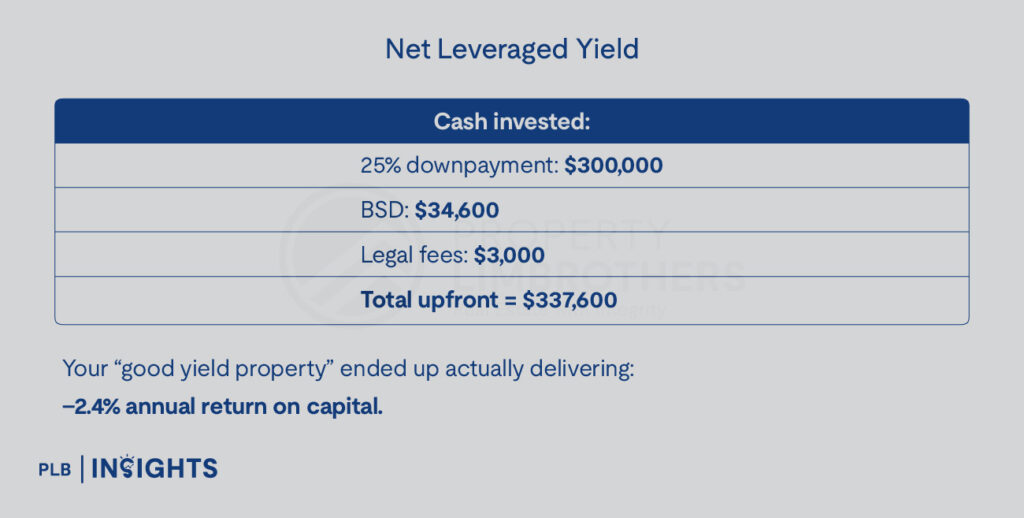

That means you are topping up:

≈ $670/month out of pocket

even though the rental yield looks like a “healthy” 4%.

Net Leveraged Yield: What You Actually Earn

What Really Matters: Cashflow > Yield

To simplify:

But the most important metric: Monthly CASHFLOW — the money you keep each month

Because only cashflow keeps you alive in a high-mortgage environment.

Capital appreciation helps you five to ten years later, cashflow determines whether you can survive until then.

Singapore Rule of Thumb

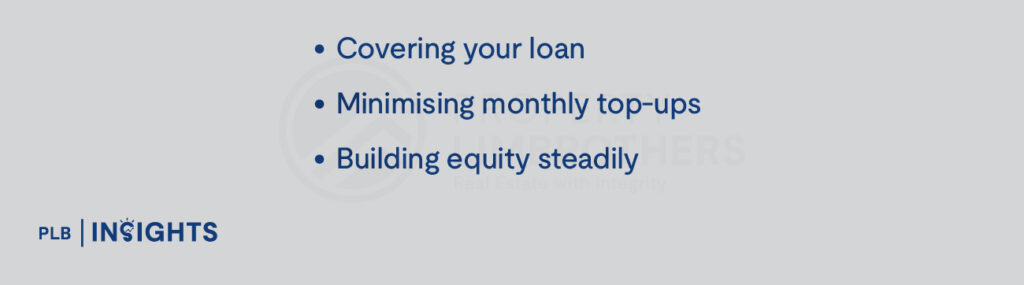

A good rental investment hits this balance:

If this holds, you’re:

And always keep: 3–6 months of mortgage instalments as a safety buffer for vacancies or unexpected issues.

Conclusion

Even in Singapore’s strong rental market, “4% yield” usually doesn’t mean profit.

Once you factor in property tax, maintenance fees, and mortgage payments, landlords may still see negative cashflow, especially with higher interest rates.

A good Singapore property investment isn’t defined by yield. It’s defined by sustainable cashflow that keeps you afloat until the property is truly yours.

Stay Updated and Let’s Get In Touch

Should you have any questions, do not hesitate to reach out to us!