In mid-2024, Beijing unveiled a sweeping ¥300 billion (~$53.07 billion) facility to revive its embattled property sector, alongside expanded credit support and repurposing of unsold inventory into social housing. That same effort was part of a broader ¥4 trillion (~$716 billion) credit push for vetted housing projects.

Now, one year on, with over a dozen policy tools still in play, it’s timely to ask—has it worked?

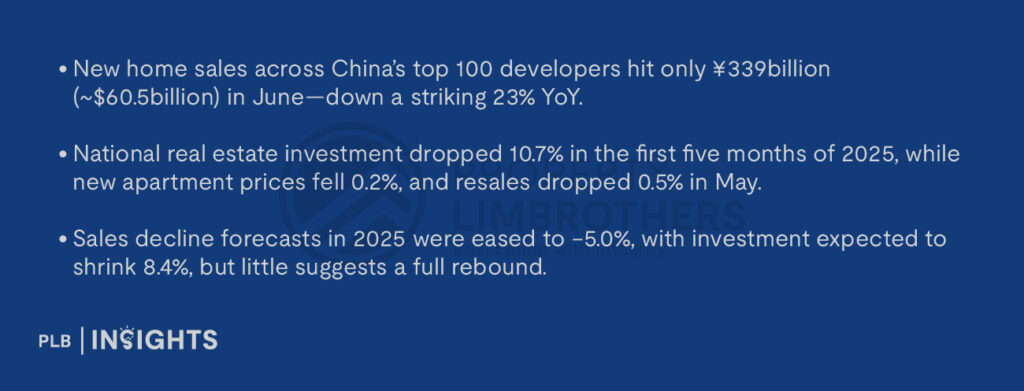

Recovery? More Like a Pause

Recent data show mixed, mostly underwhelming outcomes:

In short: signals jitter upward at times—especially in Tier-1 cities—but overall the “recovery” remains shallow and fragile.

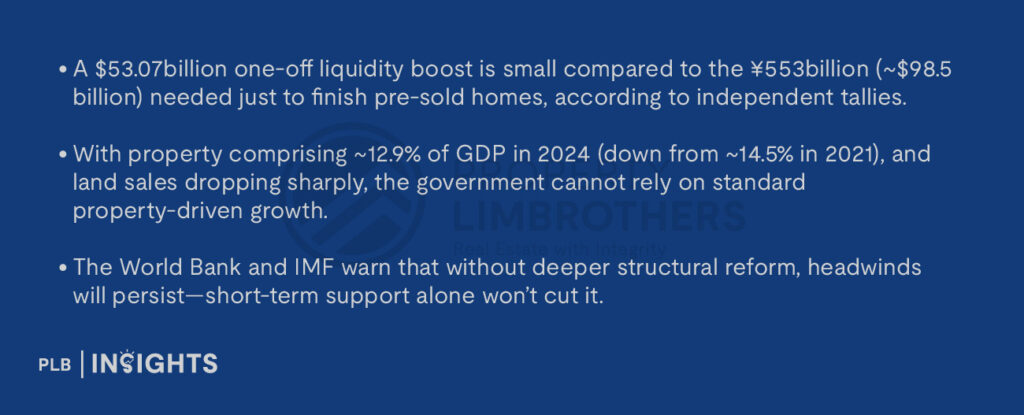

Why Bailouts Have Fallen Short

Three key reasons explain the subdued outcomes:

Massive Oversupply

Months of housing supply that took ~20 months to clear in key cities has recently fallen to 12.5 months—but that’s still elevated.

Lingering Weak Demand

Mortgage boycotts continue in smaller cities, reflecting buyer mistrust. Nationwide demand hasn’t recovered, thanks to population stagnation and cautious consumer sentiment .

Developer Distress

Even major firms like Vanke and Country Garden are under constant scrutiny, struggling with liquidity and debt restructuring—the former facing potential state intervention, the latter restructuring US$11.6 billion offshore debt in early 2025.

Beijing’s Bigger Dilemma

Spillover Impact on Singapore

So how does this matter to Singapore? Here are four key channels:

Capital Re-routing

Chinese capital that once sought high returns in domestic property might instead look abroad. While Singapore attracts institutional investments, there’s no evidence yet of a rush—only a gradual tilt toward safer, more liquid South East Asias markets.

Developer Strategy & Supply Chains

Major Singapore-listed developers with China ties, like CapitaLand and CDL, have grown more cautious. Their 2025 annual reports cite China exposure risk and hint that onshore project approvals are being purposely reduced—freeing up capital for regional investments instead.

Commodities & Construction Costs

Though China remains a major importer of steel and cement, current commodities markets show demand remains subdued. That helps Singapore’s construction sector keep input costs stable—but if China ever resumes large-scale building again, materials prices could spike.

Investor Sentiment & Safe-Haven Appeal

Stagnation—and further warnings from Goldman Sachs of potential 10% more price drops through 2027—enhances Singapore’s appeal as a more stable, transparent alternative, particularly in luxury and prime housing segments.

Singapore Market Outlook

Summary: What’s Next?

Final Take

The “bailout” of 2024 did arrest the fall—but it did not produce a full rebound. Instead, China remains trapped in a slow drift, with property still a drag on economic growth, confidence, and urban planning.

For Singapore, this means both caution and opportunity: cautious due to external shocks, but opportunistic if capital and demand figuring new regional patterns. As long as global interest rates stay higher for longer, both markets will remain intertwined—but in different configurations.

If you’re navigating today’s uncertain market and want to better understand how global shifts—from China’s slowdown to rate expectations—could affect your property journey in Singapore, our consultants are here to help. Click here to speak with our team and explore strategies tailored to your investment or homeownership goals.